This is just a reflection of evaluating the long-term prospect of a company.

As we all know, Zoom has been a huge successful company, boosted by the good timing of the covid pandemic. It has an easy-to-use video communication product with good overall quality. Its revenues has been growing strongly, even after the peak of the pandemic (as I wrote this in March 2022). So what can go wrong?

Well, I worry about the competition. In particular, I have been using tools from Google, Microsoft and GotoMeeting, and guess what, they are all very good.

In particular, I find myself using more and more Google Meet. Its visual aspects seems slightly more appealing, and more importantly, it is FREE! It integrates seamlessly with Google calendar, which I rely on. So it is really a hidden force to be reckoned with (hidden in the sense that Google does not make any money out of this product).

So I am concerned if Zoom will become a “one-trick pony”, and will be obsolete in a few years. Of course, this is just a guess. I could be totally wrong. In fact, I was wrong about Zoom right when the pandemic hit. I thought Google and Microsoft would easily roll out video conferencing products to beat Zoom in 2020, but they did not. And Zoom took over the world like wildfire in 2020. And in 2021.

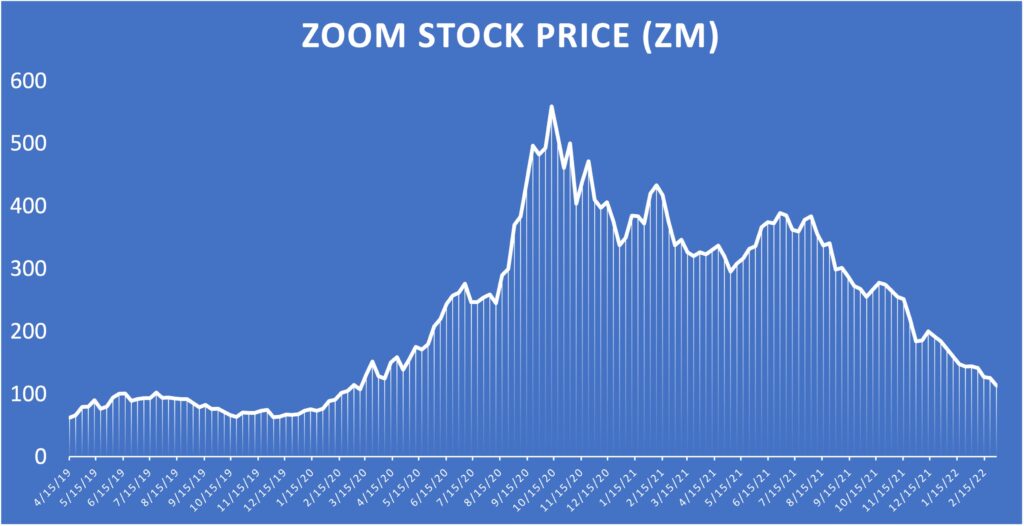

But I have to say I was right about one thing: I have always thought its stock price will fall from its 2020 high. That it did. It is now back to the level of its IPO as of its writing (much better than Peloton, which is another story for another day).

So the question is: How defensible is Zoom’s competitive advantage with the competitors catching up? Will it be another Blackberry story in 5 years?

That is what is interesting about business. You never know what is going to happen.